US Stocks

US Stocks US Options

US Options

The Post-Election Volatility Surface Realignment

Cross-asset volatilities which had had been elevated at 90+ percentile highs for the last month were crushed as the resolution of the US Presidential Elections and continued FOMC rate moderation catalyzed a cross-asset risk-on sentiment and normalized the implied volatilities of the major asset classes towards their historical average levels. Learn more in this week's Macro Volatility Digest.

AuthorWebull Learn

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- Cross-asset volatilities which had had been elevated at 90+ percentile highs for the last month were crushed as the resolution of the US Presidential Elections and continued FOMC rate moderation catalyzed a cross-asset risk-on sentiment and normalized the implied volatilities of the major asset classes towards their historical average levels.

- The conclusion of the US elections tempered implied volatilities across the developed and emerging markets including, China, the target of Trump’s tariff ire. (Implied vols on FXI have fallen 6 vol pts post-Elections to 31 despite the China ETF’s -3.5% price pullback over the same time period.) In the US, the 7 pt VIX® Index fall (to 15) represented the largest one-week VIX decline since the US reopened its borders in Dec 2021 after a nearly 2-year Covid lockdown. Interestingly, the VIX move over the course of the week (SPX® +4.65%, VIX +7pts) was remarkably well anticipated by the unusually steep skew gradient established prior to the elections. 1M S&P skew has now flattened from its 98th %ile highs to 60th %ile. Vol-of-vol has likewise compressed from its 96th %ile highs with the VVIX Index falling 34 pts to 87 (57th %ile).

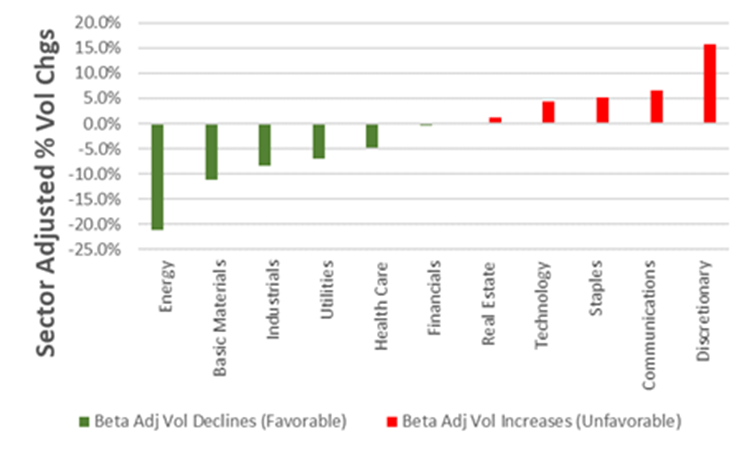

- Exhibit 3 assesses the Trump Trade at a sector level from the perspective of the volatility markets. This analysis shows the Post-Election market beta adjusted volatility premium/ discount currently priced into short term options. (i.e., a decline shows that the market neutral volatility reaction to the Elections was better than expected after accounting for market beta and vice-versa.) Accordingly, post-Elections sector trading suggests volatility traders anticipate a Trump administrative will herald a favorable outlook for the Energy, Materials & Industrials sectors and a relatively less favorable outlook for Communications & Discretionary stocks.

Chart: Volatility Traders Anticipate a Trump Administration Will Hearld a Constructive Outlook for Energy & Materials

Source: Cboe, Bloomberg

0

0

0

All investments involve risks and are not suitable for every investor. The value of securities may fluctuate, and as a result clients may lose more than their original investment. Margin trading increases the risk of loss and clients’ losses may exceed the deposits paid. The past performance of a security or financial product does not guarantee future results or returns. While diversification may help spread risk, it does not assure a profit or protect against loss in a down market.

This information is provided for general educational purposes only and does not constitute financial advice as defined in the Financial Advisory and Intermediary Services Act, 2002. It does not take into account, the financial situation, investment objectives, or particular needs of any individual investor. Unless expressly stated otherwise, transactions are executed on an execution-only basis, and no assessment of suitability or appropriateness is performed.

Certain financial products, trading features, or strategies described in this learning centre may not be available in all jurisdictions and may not be offered to clients in South Africa. Availability is subject to applicable laws, regulatory approvals, and the terms of service of the relevant Webull entity. Investors should carefully consider their objectives and risks and seek independent professional advice where appropriate before investing.

Share your ideas here…

All Comments

Following

Post

Wefolios